Prediction of regionalized car insurance risks based on control variates

Abstract

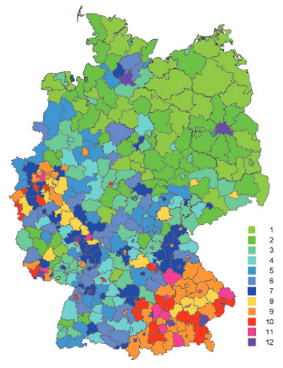

We show how regional prediction of car insurance risks can be improved for finer subregions by combining explanatory modeling with phenomenological models from industrial practice. Motivated by the control-variates technique, we propose a suitable combined predictor when claims data are available for regions but not for subregions. We provide explicit conditions which imply that the mean squared error of the combined predictor is smaller than the mean squared error of the standard predictor currently used in industry and smaller than predictors from explanatory modeling. We also discuss how a non-parametric random forest approach may be used to practically compute such predictors and consider an application to German car insurance data.

Type

Publication

Stat. Risk Model.